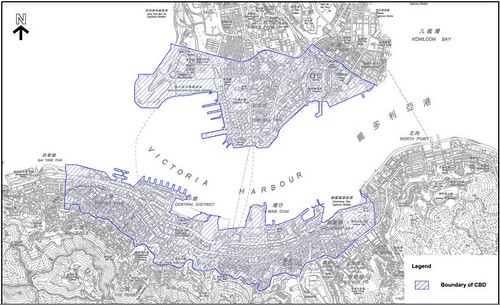

圖:香港2030對中心商務區的定義

政府早前推出了保育中環計劃,美其名要將中區一帶的古物古蹟列入保育項目,實際上卻是借其名來進行商業買賣。其中,中區政府合署西翼位於終審法院和聖約翰座堂等法定古蹟群之中,賦有深遠的歷史意義,政府卻計劃把西翼拆卸,並挖去半座山來出售作甲級寫字樓和大型購物商場,當中的理據疑點重重。有關賣山建寫字樓可處理寫字樓不足的說法,更是讓人費解,本文原作者撰文分析了甲級寫字樓於各區的發展情況,重新審視賣山方案的不合理性。(政府山系列文章可見此)

譯文:

面對中區(Central)和中心商務區(CBD)甲級寫字樓短缺的情況,普遍的出路是分散甲級寫字樓分佈。但現在竟然有規劃者提出,拆卸中區政府合署西翼以舒緩短缺,這是天真和誤導的說法。現實是,拆卸西翼所得的28,500平方米甲級寫字樓樓面面積,相對於整體供應而言,只是杯水車薪。

集中與分散的發展

由於維多利亞港已經不會進行任何填海工程,房地產行業早已意識到中區缺乏合適的(甲級寫字樓)土地供應。以下數據亦顯示,分散甲級寫字樓分佈的做法,已經在過去二十年來,成功地回應香港由製造業基礎過渡為國際服務業中心所需的條件。

2011年3月12日,發展局局長和規劃署署長在一個有關寫字樓發展的研討會上,提供了非常有趣的資料,亦表明了香港截至2010年底,在此議題上的立場。

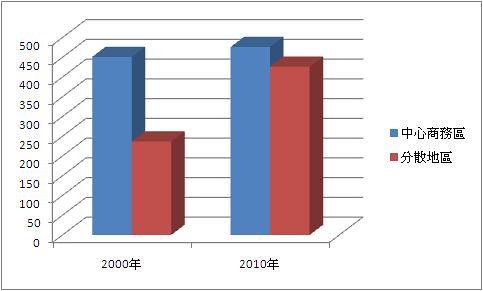

圖:過去十年中心商務區與分散地區的比例

現時中心商務區(CBD)的定義涵蓋了港島北岸(由上環至銅鑼灣)和九龍半島(沿著西九龍到紅磡)。

若追溯到1995年,當時大約有400萬平方米甲級寫字樓面積等量地分佈於中心商務區和分散地區。至2000年共有451萬平方米(66%)位於中心商務區,237萬平方米(34%)位於分散地區。到2010年,中心商務區的甲級寫字樓面積只是上升到476萬平方米(53%),而分散地區則有426萬平方米(47%)。因此,在過去十年近乎有200萬平方米甲級寫字樓面積落成於分散地區,以滿足持續的需求。

飽和了,還要再加?

從另一角度而言,自過去到將來,中區都會出現甲級寫字樓供應不足的情況,這反映在極高昂的租值交易上。然而,隨著現時市場提供分散地區的可能,租值約為中區的1/3至1/2,讓租戶能夠真正地擁有不同地點和價錢的選擇。

今時今日,中區的辦公室空間已經到達了飽和點,一個明顯的例子是,任何工作日當中,都會見到擠塞又污染的馬路已經無法處理現時的交通流量,行人走過於狹窄而無法提供舒適的行人通道,地下鐵過於擁擠,連午飯時間都難以找到地方。簡而言之,現有的基礎建設已經無法支撐任何人流的增加。

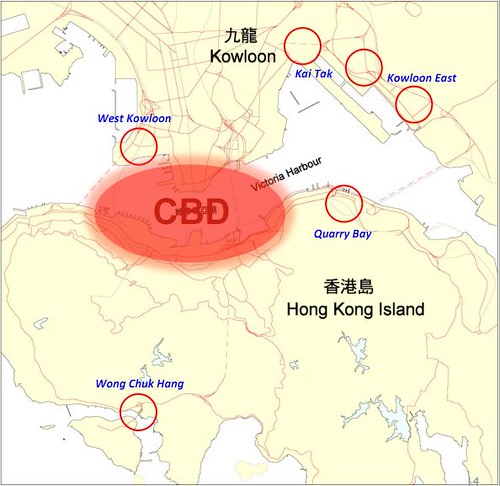

圖:政府文件建議中的辦公室樞紐

為何出賣政府山?

財政司司長於2011-12年度的財政預算案演說中,表示「為提升競爭力,我們必須維持穩定及足夠的甲級寫字樓供應,並更積極地進行土地用途規劃、城市設計和地區改善,以及提供更便捷的交通網絡,發展新的優質辦公室群。」這句說話清楚表明,中區和中心商務區都不可能是(甲級寫字樓的)供應來源,因此需要另覓地方,而事實上,這是已經發生中的事情。九龍東(包括九龍灣、牛頭角、觀塘)是一個很好的例子,那裡共有130萬平方米甲級寫字樓面積,而且有6個劃作商業用途(commercial/business)的政府賣地項目,售後共會提供35萬平方米甲級寫字樓面積。此外,那裡共有68公頃剩餘的工業用地現時規劃作「其他指定用途」(商業)用途,假設地積比率為10,將會陸續提供接近600-700萬平方米辦公室空間。其他例子如啟德建議中的辦公室樞紐,證明了香港現時或將來的甲級寫字樓供應都十分充裕。

最後,如果辦公室的即時供應如此重要,為何不重新考慮將美利大廈出售作辦公室用途?它本來的設計和建築目的便是辦公室,而非酒店。現時美利大廈建築面積42,560平方米,比規劃中的西翼項目還要大,而當中富有特色的窗口設計亦於1994年贏得了「建築物能源效益獎」的優異獎,若能進一步提升到香港建築環境評估證書計劃(HK BEAM),或領先能源與環境設計(LEED)的環境標準,將能夠仿傚灣仔華潤大廈的改善工程,從而達到甲級寫字樓水平。

相關連結:

香港辦公室發展研討會簡報及錄像

政府山計劃

原文:香港大學房地產及建設系客座教授Roger Nissim

註:標題及副標題為譯者所外加

Y/H4/6 CGO – Response to Comments

Decentralization of Grade A offices is already the solution to the lack of space in Central and the Central Business District (CBD) generally so the suggestion by the planners that 28 500sq.m of Grade A office that the proposed West Wing site will provide will go towards alleviating the shortfall of Grade A space is Central is both naïve and misguided as it represents the proverbial ‘drop in the bucket’ in the context of the overall supply.

Given that there will be no more reclamation taking place in Victoria Harbour the lack of supply of suitable sites in Central has long been recognized by the property industry and as the following data will demonstrate decentralization of offices has been successfully taking place over the past two decades in order to meet Hong Kong’s requirements during its transition from a manufacturing base to an international service centre.

At a Seminar on Office Development held on 12th March 2011 both the Secretary for Development and the Director of Planning produced some very interesting information on this subject setting out the position in Hong Kong as at the end of 2010.

Their definition of CBD covers the north shore of HK Island from Sheung Wan through to Causeway Bay and on the Kowloon peninsula from West Kowloon along to Hung Hom.

Going back to 1995 there was about 4m sq.m of Grade A office space split equally between the CBD and decentralized locations. By 2000 there was 4.51m sq.m, 66% of such GFA within the CBD with 2.37m sq.m, or 34%, elsewhere. Arriving at 2010 the figure for the CBD had only risen to 4.76m sq.m ,now 53%, whereas decentralized offices had grown to 4.26m sq.m or 47% of the total stock of Grade A offices. So in the last decade nearly 2m sq.m of Grade A office has been built in decentralized locations in order to meet the ongoing demand for such quality office space.

Put another way there has been, and there always will be, a shortfall of supply in Grade A office supply in Central. This is reflected in the extremely high rentals that are being charged and paid. However with the market now providing decentralized alternatives at prices a third or half of those in Central the end users now have a genuine choice of where to locate and what price to pay and are indeed exercising such choices.

In any event there is a good case for arguing that today Central has reached saturation point as regards the provision of office space. A casual observation on any working day will reveal congested and polluted roads that cannot cope with the existing volume of traffic, footpaths that are too narrow to cater for comfortable pedestrian movement, journeys on the MTR that are unpleasantly over-crowded and the difficulty in finding a place to eat at lunch time. In short the existing infrastructure cannot support the intake of any more people.

In his 2011-12 Budget Speech the Financial Secretary said ‘ To enhance our competitiveness we must maintain a steady and adequate supply of Grade A offices and strive to develop new high grade office clusters through land use planning, urban design, area improvements and the provision of better transport networks.’ This statement clearly recognizes that there is virtually no possibility of major supply coming from within the CBD and certainly not in Central so there is a need to look elsewhere and indeed this is what is already happening. A good example is Kowloon East that covers Kowloon Bay, Ngau Tau Kok and Kwun Tong. Already there is 1.3m sq.m of Grade A office space there. There are 6 government sale sites for commercial/business use that when sold could generate a further 0.35m sq.m and overall there are 68 hectares of redundant industrial land now zoned for OU(Business) which, assuming a plot ratio of 10, will over time produce close to 6-7m sq.m of new office space. There are other examples such as the proposed office node around Kai Tak so overall Hong Kong is well placed to meet its present and future needs for Grade A offices.

One final thought, if the immediate supply of office space is so important, is why not reconsider the use of Murray Building and offer it for sale as offices, for which it was originally designed and built, rather than hotel? The existing gfa is 42560sq.m which is greater than planned for the West Wing site. The buildings characteristic window design won a Certificate of Merit of the Energy Efficiency Building Award in 1994 and further upgrading to HK BEAM or LEED environmental standards could be carried along the lines of the work currently being done on the China Resources Building in Wanchai to achieve Grade A quality.

Roger Nissim

Adjunct Professor,

Real Estate & Construction Dept,

HKU

13th April 2011